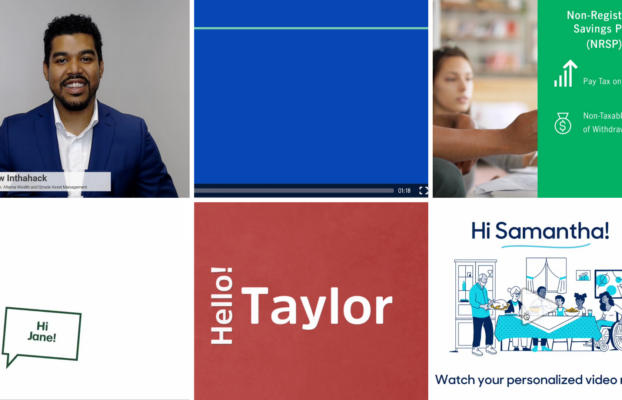

Transform ordinary data into compelling videos that motivate your customers, clients or prospects to take the desired action. No video production experience required.

Digital Experiences

Turn lacklustre campaigns and websites into sizzling digital solutions that increase conversion rates and boost ROI. Our marketing experts know how.

Strategy & Consulting

Revitalize your digital presence into a CX powerhouse. Together with our expertise in industry best practices, competitive review insights and technical wizardry, we’ll make it happen.